2023 September Stewardship Advocate

AG CARBON MARKETS

Ag carbon markets are in their relative infancy but are expected to grow significantly over time. The ag carbon market size in the United States is around $5 billion currently and some estimates push the value to $250 billion by 2050. The desire to mitigate greenhouse gas (GHG) emissions has existed for several years and is prevalent in many industries and countries. Mechanisms to regulate carbon include carbon taxes and carbon markets, which can be regulated or voluntary. Policy initiatives or regulatory bodies are needed to create either a carbon tax or regulated carbon market. Voluntary markets develop organically without regulatory oversight. All programs currently available to farmers would be classified as voluntary carbon markets.

Voluntary programs offering carbon offsets1 to farmers have become more common in the US. In the last few years, the number of companies offering these programs has increased significantly. The push for carbon markets has largely come from public interest in addressing changes in weather patterns and climatic factors. Many in the public are looking for goods and services that are or claim to be less impactful to the environment. As a result, companies are taking actions to lower their GHG emissions and appear more attractive and sustainable to shareholders and consumers. And one way to do this is to buy carbon offsets from farmers.

Most carbon program incentives involve farmers adopting practices that have been shown through research and modeling to increase the carbon in the soil or reduce emissions associated with farming. Planting cover crops, reducing tillage to strip-till or no-till, and improving nitrogen management are practices commonly promoted by carbon programs. They offer incentives/compensation to farmers for agreeing to participate in the program by implementing a new conservation practice in fields that have not had practices used on them in the recent past. One of the common criticisms of carbon programs is that farmers who are early adopters of a practice are not eligible for carbon payments on acres where they have used that practice for years or even decades. For example, growers who no-till all of their acres are not eligible for carbon payments on those acres.

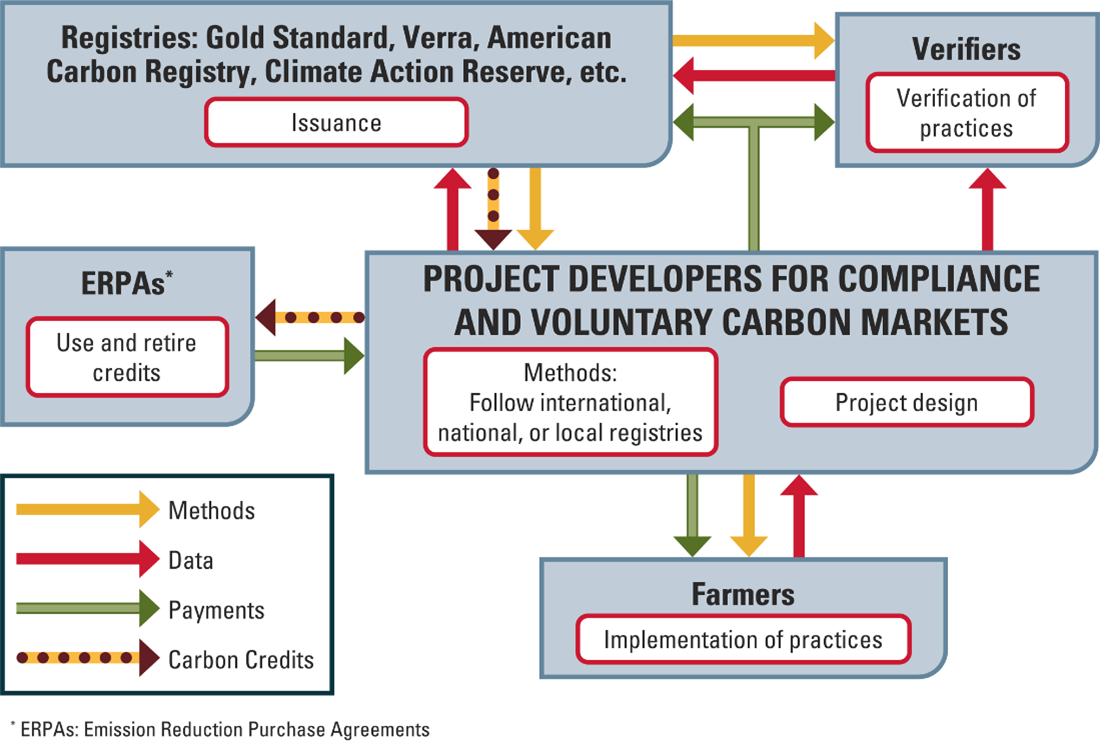

Although the carbon programs offered to farmers today are not uniform, most of them have similar components in the value chain. The components are shown in Figure 1 and include sellers (farmers), project developers, 3rd party verifiers, and carbon registries. The registries issue carbon offsets and act on behalf of companies that are buying the credits to reduce their carbon footprint.

Ag carbon programs vary widely in how farmers are compensated, the length of the contract, how carbon sequestration is quantified, how verification occurs, specifics on regions/practices that are allowed in the program and how new a practice must be to be eligible for the program (additionality). These differences between programs make it difficult to easily compare programs side by side. This makes it important for farmers to inquire about compensation, quantification, outcome-based or practice-based and other relevant topics to ensure a proposed program makes sense for their operation.

Iowa Corn Promotion Board is developing a white paper that delves into all of the aspects of ag carbon markets, including a series of questions for farmers to ask carbon program providers to ensure they are aware of the how a program operates before signing a contract.

1 A carbon offset is a reduction or removal of emissions of carbon dioxide or other greenhouse gases made in order to compensate for emissions made elsewhere. A carbon credit or offset credit is a transferrable instrument to represent an emission reduction of one metric ton of CO2, or an equivalent amount of other greenhouse gases.

FARMER TO FARMER: MARK MUELLER

In the July edition of the Stewardship Advocate, Mark Mueller shared information about his operation, including his commitment to cover crops and being an original participant in the Soil Health Partnership (SHP). He has continued his participation in the SHP for the last nine years. The photo below shows the clear demarcation of the cover crop strips in this year’s soybean field. The dark green strips are where Mark has grown cover crops every year since 2015 and the yellow strips have not had cover crops. We will follow the progress of this field and report on the yield differences after harvest.

LATEST INFORMATION

Rise of the Spray Drone | (thedailyscoop.com)

Enhance Soil Health in Your Fields: https://farmersforsoilhealth.com/

Risk–Reward: Tar Spot Tolerant Versus Susceptible Hybrids | The Scoop (thedailyscoop.com)

Upcoming Events

October 4: Eileen Kladivko, Purdue University; Iowa Learning Farms webinar; Drainage for the Long-Haul: Impacts on Crop Yields, Soil Health, and Water Quality; Events – Iowa Learning Farms

October 11: Craig Clarkson, ISG; Iowa Learning Farms webinar; Market District Green Infrastructure; Events – Iowa Learning Farms

October 11: Presenter: Jingyi Tong – PhD student and graduate research assistant, Department of Economics, majoring in Agricultural Economics; Topic: Landowners Matter Too: Accelerating Adoption of In-field and Edge-of-field Nutrient Reduction Practices through Better Engaged Landowners; https://go.iastate.edu/ZMTZTZ

Share This Article

Related Articles

The March 2025 Stewardship Advocate highlights the Environmental Protection Agency (EPA) published the herbicide strategy

The February 2025 Stewardship Advocate highlights the Iowa Nitrogen Initiative new Decision Support Tool.